YOU’VE got £50,000 sitting there.

Maybe you sold a business, inherited it, saved like a maniac, or finally cashed in on something.

Now the question everyone asks: “How do I invest £50,000 in the UK?”

The banks, the “experts” and your mates will all give you the same safe, boring, broke answer.

I’m not here to give you safe.

I went from £50k in debt and skint to a deca-millionaire by 31.

Here’s the brutal truth – there are two ways to invest £50k in the UK right now.

The broke way (what 95% of people do).

The rich way (what actually builds generational wealth).

Let’s compare them with real numbers, no fluff, and a 15-year projection so you can see the difference with your own eyes.

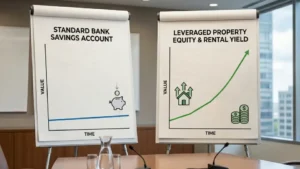

The Broke Way: Stick it in a savings account (or overpay the mortgage)

You do the “responsible” thing.

You pop the £50k in a high-interest savings account or use it to overpay your mortgage.

- Annual return: ~4.5% (best easy-access rates right now)

- You stay “safe”

- You pay tax on the interest (unless in an ISA)

- Inflation quietly eats 3%+ of it every year

Result after 15 years?

Your £50k grows to around £103,000 (compounded at 4.5%).

You feel virtuous.

You have a slightly bigger number in the bank.

But you’re still trading time for money and your money is barely beating inflation.

The Rich Way: Use it as a deposit on leveraged property

You treat the £50k as leverage, not a finish line.

Put it down as a 20% deposit on a £250,000 buy-to-let property (perfectly doable in many UK towns right now).

- Tenant pays the mortgage

- You get rental income

- Property grows in value

- You use other people’s money (the bank’s) and inflation to make your £50k work 4-5x harder

Realistic UK numbers I use in my own portfolio:

- Rental yield: 6-7% gross (after costs ~5% net cashflow)

- Annual property growth: 5% (conservative long-term UK average)

- Mortgage at 5% (interest-only to maximise cashflow)

Result after 15 years?

Your original £50k deposit is now worth £580,000+ in equity (property at ~£530k minus remaining mortgage).

Plus you’ve pocketed £120,000+ in cumulative net rental cashflow (reinvested or spent).

That’s over 5x the broke way.

15-Year Projection: Broke Way vs Rich Way

| Year | Broke Way (£50k in savings @4.5%) | Rich Way (£50k deposit on £250k BTL property) |

| 0 | £50,000 | £50,000 (deposit) |

| 5 | £62,800 | £185,000 equity + £35k cashflow |

| 10 | £79,000 | £310,000 equity + £75k cashflow |

| 15 | £103,000 | £580,000+ equity + £120k+ cashflow |

(The rich way numbers are conservative examples – real UK property deals I’ve done and seen in my portfolio beat this. – Past performance is no guarantee of future results)

This is why I remortgaged my own home to interest-only and used the freed-up cash to buy more property.

This is why I tell people: stop paying the bank early. Make the bank work for YOU.

Not financial advice. Do your own research or speak to a qualified adviser. Past performance is no guarantee. Property involves risk, tax implications and costs.

The Bottom Line

The broke way feels safe.

The rich way feels scary at first.

But what’s right isn’t easy and what’s easy isn’t right.

You reject that which you are NOT. You attract that which you ARE.

In order to change your money, you need to change your mind.

If you don’t risk anything, you risk everything.

Most people will read this, nod, and still do the broke way.

The ones who actually get rich? They take the £50k and make it work like a deca-millionaire would.

If you want the exact step-by-step systems I use to turn lump sums into multiple income streams, plus private mentoring and a community of people actually doing this…

Join my exclusive membership at Money.school right now.

We don’t just talk about investing £50k.

We show you how to turn it into £500k+ while you sleep.

Your future millionaire self is waiting.

Go get it.